- Location

- Stoneleigh

The International Grains Council (IGC) increased its forecast for global grain supply in 2021/22 by 9.0Mt yesterday, to 2,301Mt. This is a new record.

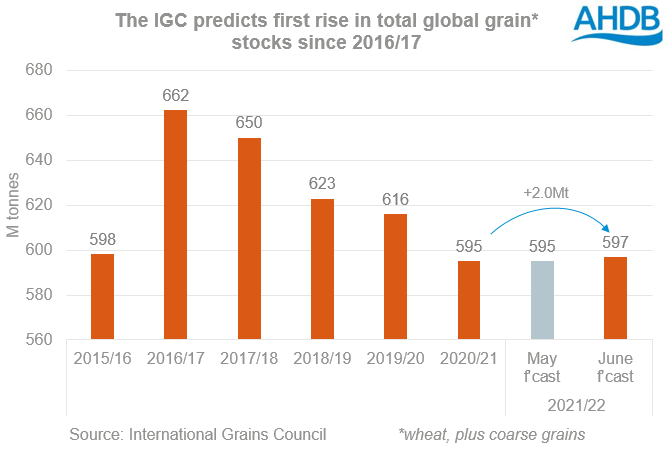

Demand also increased by 2.0Mt to 2,299Mt. The big increase in the grain crop shifts the global grain market from another deficit, to a tiny surplus (+2.0Mt). This would be the first global surplus and year-on-year rise in stocks since 2016/17.

The key change is a big (+5.5Mt) increase in Chinese maize production. But, Chinese maize imports in 2021/22 are only trimmed by 1.0Mt.

The global wheat crop in 2021/22 is pegged at 789.4Mt, 0.7Mt lower than in May. There are increases to the wheat crops in several top exporting countries, including Russia (+2.2Mt), Australia (+1.7Mt), the EU-27 (+1.4Mt), and Ukraine (+1.0Mt). But, there were more than offset by decreases for others, such as India (-2.0Mt) and Kazakhstan (-1.1Mt).

It is worth noting that the estimate of total grain stocks level at the end of 2020/21 is 595.0Mt. This is 4.0Mt lower than in the May report, due to tighter grain supplies in 2020/21. The Brazilian crop is -3.5Mt lower, plus there is higher domestic and export demand for US maize.

The impact on prices?

The predicted stocks are still very low. This leaves little room for error if supply gets disrupted. Overall, the IGC forecasts add to the picture that the supply might just be enough in 2021/22.

The critical weeks for US maize crops are beginning and the US maize crop accounts for more than 16% of total global grain output. So, the weather across the Midwest in the weeks ahead could have a considerable bearing on where prices go next. Hot weather in July would threaten the tiny global grain surplus and likely push up prices once more.

But, if there isn’t challenging weather, especially in the US, global grain prices are likely to drift lower in the coming weeks.

IGC predicts first global grain surplus since 2016/17

Join the 3.6K people who subscribe to our Grain Market Daily publication here - https://ahdb.org.uk/keeping-in-touch

Demand also increased by 2.0Mt to 2,299Mt. The big increase in the grain crop shifts the global grain market from another deficit, to a tiny surplus (+2.0Mt). This would be the first global surplus and year-on-year rise in stocks since 2016/17.

The key change is a big (+5.5Mt) increase in Chinese maize production. But, Chinese maize imports in 2021/22 are only trimmed by 1.0Mt.

The global wheat crop in 2021/22 is pegged at 789.4Mt, 0.7Mt lower than in May. There are increases to the wheat crops in several top exporting countries, including Russia (+2.2Mt), Australia (+1.7Mt), the EU-27 (+1.4Mt), and Ukraine (+1.0Mt). But, there were more than offset by decreases for others, such as India (-2.0Mt) and Kazakhstan (-1.1Mt).

It is worth noting that the estimate of total grain stocks level at the end of 2020/21 is 595.0Mt. This is 4.0Mt lower than in the May report, due to tighter grain supplies in 2020/21. The Brazilian crop is -3.5Mt lower, plus there is higher domestic and export demand for US maize.

The impact on prices?

The predicted stocks are still very low. This leaves little room for error if supply gets disrupted. Overall, the IGC forecasts add to the picture that the supply might just be enough in 2021/22.

The critical weeks for US maize crops are beginning and the US maize crop accounts for more than 16% of total global grain output. So, the weather across the Midwest in the weeks ahead could have a considerable bearing on where prices go next. Hot weather in July would threaten the tiny global grain surplus and likely push up prices once more.

But, if there isn’t challenging weather, especially in the US, global grain prices are likely to drift lower in the coming weeks.

IGC predicts first global grain surplus since 2016/17

Join the 3.6K people who subscribe to our Grain Market Daily publication here - https://ahdb.org.uk/keeping-in-touch