- Location

- Stoneleigh

This season (2021/22) the European Union is set to export 30Mt of wheat, according to the EU commission. Data released by the commission yesterday showed EU exports of common wheat totalled 6.53Mt from 01 July to 19 September.

So far, EU exports have been dominated by Eastern European states. This season, 35% of common wheat exports from the EU have originated in Romania, with a further 18% originating in Bulgaria. This is not a huge surprise; Romania has been a key origin in international wheat tenders so far this season. Production in the South East European state is up 5.9% on the five-year trim average, at 10.1Mt.

Exports from the EU have broadly kept up with the pace required to meet the 30Mt forecast. But, EU wheat prices, and Paris milling wheat futures, will need to remain competitive if the export outlook is to be met.

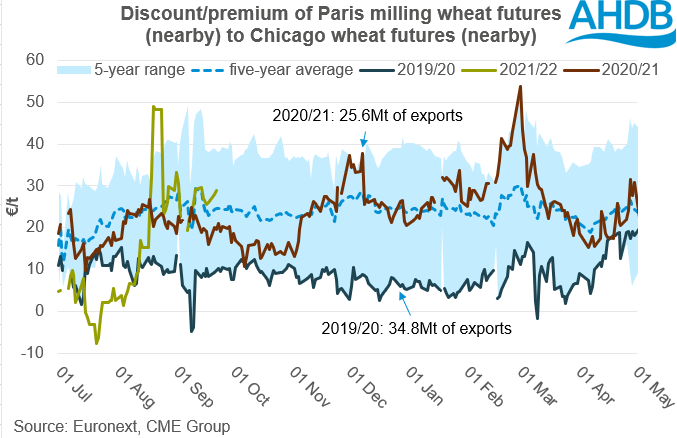

In euro terms, Paris wheat futures are at a less competitive point than they were at the beginning of the 2021/22 season. The premium of nearby Paris milling wheat futures to nearby Chicago wheat futures is around the five-year average level. While exports have remained strong in recent weeks, the premium of Paris over Chicago is currently more than it was last season. Total EU common wheat exports reached just 25.6Mt last season. If trade is to reach the level required, then Paris milling wheat futures may need to reduce their premium to Chicago wheat futures, the global benchmark for wheat pricing.

UK pricing tends to follow the trend seen in Paris milling wheat futures, effected by the exchange rate. As such, any reduction in the premium of Paris milling wheat futures over Chicago wheat futures is likely to impact UK markets.

If Paris milling wheat moves lower to find demand, then we could see UK markets move lower also. One major caveat is the shape of the grain market globally this season. With reduced competition for exports this season; reduced Russian, Canadian and US exports, Paris futures may not need to reduce the premium over Chicago to the same degree as in previous seasons to capture demand.

So far, EU exports have been dominated by Eastern European states. This season, 35% of common wheat exports from the EU have originated in Romania, with a further 18% originating in Bulgaria. This is not a huge surprise; Romania has been a key origin in international wheat tenders so far this season. Production in the South East European state is up 5.9% on the five-year trim average, at 10.1Mt.

Exports from the EU have broadly kept up with the pace required to meet the 30Mt forecast. But, EU wheat prices, and Paris milling wheat futures, will need to remain competitive if the export outlook is to be met.

In euro terms, Paris wheat futures are at a less competitive point than they were at the beginning of the 2021/22 season. The premium of nearby Paris milling wheat futures to nearby Chicago wheat futures is around the five-year average level. While exports have remained strong in recent weeks, the premium of Paris over Chicago is currently more than it was last season. Total EU common wheat exports reached just 25.6Mt last season. If trade is to reach the level required, then Paris milling wheat futures may need to reduce their premium to Chicago wheat futures, the global benchmark for wheat pricing.

UK pricing tends to follow the trend seen in Paris milling wheat futures, effected by the exchange rate. As such, any reduction in the premium of Paris milling wheat futures over Chicago wheat futures is likely to impact UK markets.

If Paris milling wheat moves lower to find demand, then we could see UK markets move lower also. One major caveat is the shape of the grain market globally this season. With reduced competition for exports this season; reduced Russian, Canadian and US exports, Paris futures may not need to reduce the premium over Chicago to the same degree as in previous seasons to capture demand.