- Location

- Stoneleigh

Yesterday, Dec-21 Paris wheat futures passed its 7 May peak, as the world market reacted to more negative news about world wheat supplies. The contract closed at €230.75/t, up €5.25/t from Friday.

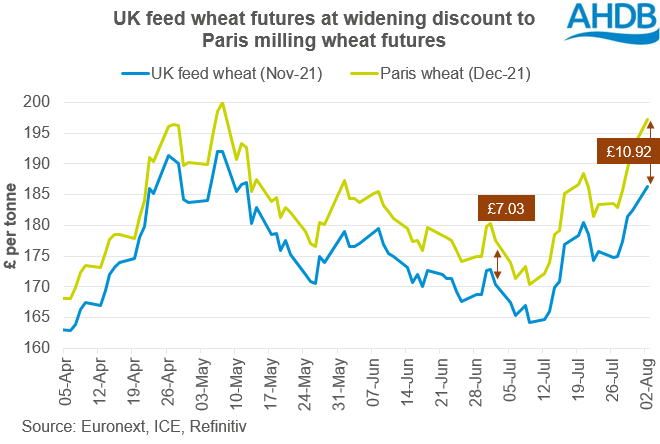

The UK Nov-21 futures price is now nearly £11/t below the Paris Dec-21 price. We usually see a discount of this size when the UK needs to export wheat. However, while UK wheat production could be around 14.9Mt this year, we are expecting animal feed and ethanol demand to rise too. This will keep the UK market tight. As a result, it’s uncertain how much wheat the UK can export this season.

Last week (Thursday-Thursday), UK delivered wheat prices rose more than the Nov-21 futures, widening the gap (or basis). This suggests that currently it’s the cash prices that are keeping exports priced out. This is likely to continue until we get some confirmation of the UK crop size and early demand trends, therefore potential export availability. In the coming weeks, expect either:

For information on price direction for crops too, make sure to subscribe to Grain Market Daily’s and Market Report from our team.

- SovEcon cut 5.9Mt from its forecast of the Russian wheat crop. The crop is now estimated at 76.4Mt. This follows official data showing the winter wheat area was 1.2Mha smaller than expected, pointing to higher winterkill. This follows a 3.0Mt cut by IKAR last week. A smaller Russian crop could reduce the volume available for export in 2021/22. The USDA currently expects Russia to be the world’s top exporter of wheat this season and ship 40.0Mt.

- The US spring wheat harvest was 17% complete by 1 August (USDA), well ahead of the five-year average (8%). Crops are in poor condition due to hot, dry conditions. Early quality results from US Wheat Associates also show lower bushel weights and higher proteins.

The UK Nov-21 futures price is now nearly £11/t below the Paris Dec-21 price. We usually see a discount of this size when the UK needs to export wheat. However, while UK wheat production could be around 14.9Mt this year, we are expecting animal feed and ethanol demand to rise too. This will keep the UK market tight. As a result, it’s uncertain how much wheat the UK can export this season.

Last week (Thursday-Thursday), UK delivered wheat prices rose more than the Nov-21 futures, widening the gap (or basis). This suggests that currently it’s the cash prices that are keeping exports priced out. This is likely to continue until we get some confirmation of the UK crop size and early demand trends, therefore potential export availability. In the coming weeks, expect either:

- UK wheat futures to track Paris futures more closely to close the gap.

- Or UK delivered prices to hold or widen their premiums over UK futures.

For information on price direction for crops too, make sure to subscribe to Grain Market Daily’s and Market Report from our team.